Attention: GST verification now requires in-person biometric authentication.

Important Update: New Requirement for GST Registration

Dear Valued Businessmen,

The government has introduced an additional verification step for GST registration, which includes biometric authentication for Aadhaar verification. This step will be applicable in specific cases, depending on the applicant’s profile and location.

States Affected

The new process applies in various states, including but not limited to Andhra Pradesh, Gujarat, Bihar, Delhi, Karnataka, Pondicherry, Tamil Nadu, West Bengal, and Punjab.

Effective Date

This updated procedure will take effect starting 6th September 2024.

What Does This Mean for You?

When you submit Form GST REG-01 for registration, the next steps will vary:

- Online Authentication:

- You may receive a link to complete an OTP-based Aadhaar authentication.

- Appointment at GST Suvidha Kendra (GSK):

- If biometric verification is required, you will be directed to schedule an appointment at the nearest GSK.

Documents Required for GSK Visit

To ensure a smooth process, please bring the following documents to your scheduled appointment:

- The appointment confirmation email

- Details of your jurisdiction

- Aadhaar Card (original)

- PAN Card (original)

- Supporting original documents for your GST registration

Need Help?

If you have questions or need assistance with the updated process, our GST experts are here to guide you.

For complete details, please visit the official advisory on the GST Portal.

Streamlined GST Registration Services

- Submit your GST application within just 2 business days, starting at an affordable price of ₹499. (*Terms and Conditions Apply)

- Enjoy a seamless process for new GST registration, complete with status updates and expert help for resolving clarifications.

- Our services are designed to cater to individuals, eCommerce businesses, and government entities, ensuring every GST-related requirement is addressed.

- From CA-supervised document preparation to GSTIN registration and regular filing, we’ve got all your GST-related tasks covered.

- Expert guidance for e-invoicing, maintaining ledgers, and creating error-free GST-compliant invoices.

Need Prior Assistance For Gst Registration

List of documents needed

- Certificate of Incorporation

- PAN card of Company

- Articles of Association, AOA

- Certificate of Incorporation

- PAN card of Company

- Articles of Association, AOA

- Memorandum of Association, MOA

- Resolution signed by board members

- Identity and address proof of directors

- Digital Signature

- Director’s Proof (Any 2 from the below)

- PAN Card of LLP

- LLP Agreement

- Partners’ names and address proof

- Director’s Proof (Any 2 from the below)

- PAN Card

- Address proof of proprietor

Director's Proof (Any 2 to be shown as proof of address of a director)

- Telephone or Electricity Bill

- Bank Account Statement

- Passport

- Aadhar Card

- Driving License

- Ration Card

- Voter Identity Card

GST Registration Fees

GST REGISTRATION

- Exclusive of 18% GST*

- Application For GST Filing

- Application For Clarification

- Any Modification In GST Registration Application

- Pay Extra 1000 Rupees For Live Registration*

-

Terms & Conditions

Submit all documents within 4-6 business hours post payment. Ensure Aadhaar and PAN details match. Downtime on government portal might cause delay.

Understanding GST Registration

GST registration is the procedure through which businesses and individuals acquire a Goods and Services Tax Identification Number (GSTIN), a unique 15-digit code that makes them accountable for collecting and remitting GST in India. Mandated by the Central Goods and Services Tax Act, 2017, this registration is compulsory for entities exceeding an annual turnover of ₹40 lakh (₹20 lakh in certain special category states). GST is a comprehensive, destination-based indirect tax that consolidates various levies like VAT and excise duty. It also applies to eCommerce sellers regardless of turnover. The entire registration process is conducted online via the official GST portal. Applicants receive an Application Reference Number (ARN) upon submission, enabling them to track the status of their GSTIN issuance conveniently.

Note:

This threshold can change from state-to-state, for the latest and accurate information to get in touch with our experts today.

GST ACT

The Central Goods and Services Tax Act of 2017, implemented to streamline taxation and curb tax evasion, establishes the framework for the Goods and Services Tax (GST) levied on intra-state and inter-state supplies of goods and services in India.

Key Advantages of GST Registration

Registering under the Goods and Services Tax (GST) framework offers numerous benefits that enhance a business's credibility, streamline operations, and foster growth. Here’s how GST registration can positively impact your enterprise:

Legal Recognition

By registering for GST, your business gains legal acknowledgment as a bona fide supplier of goods or services. This not only strengthens your market reputation but also establishes your entity as a compliant, trustworthy partner in the eyes of customers and vendors.

Access to Input Tax Credit (ITC)

One of the most significant benefits of GST registration is the ability to claim Input Tax Credit. Registered businesses can offset the GST paid on purchases against the GST collected on sales. This effectively lowers the net tax payable, thereby enhancing cash flow and reducing operational costs.

Simplified Compliance

The GST system has revolutionized tax compliance by introducing a unified, digital platform for filing returns and making payments. This eliminates cumbersome paperwork, saves time, and ensures that businesses can seamlessly meet their tax obligations without unnecessary delays or errors.

Advantageous Composition Scheme

Small businesses can benefit from the Composition Scheme, which allows them to pay taxes at a lower, fixed rate. This reduces their tax burden while minimizing compliance formalities, making it easier for them to focus on growth without being overwhelmed by regulatory requirements.

Increased Threshold

Under the GST framework, only businesses with an annual turnover exceeding ₹40 lakh (or ₹20 lakh in special category states) are required to register. This higher threshold exempts many smaller enterprises from mandatory registration, offering them the flexibility to operate without additional compliance demands.

Prevention of Tax Cascading

GST resolves the long-standing issue of the cascading effect of taxes, where taxes were levied on top of taxes. By enabling seamless input tax credit across the supply chain, GST ensures that the overall tax burden on businesses and consumers is significantly reduced, leading to more competitive pricing and higher profitability.

GST Registration Eligibility and Threshold Limits

GST registration is a mandatory compliance for businesses meeting specific turnover criteria. It is essential to verify your eligibility before initiating the registration process. Entities previously registered under Pre-GST laws must also migrate to GST. Here’s an overview of the threshold limits and their applicability:

| Aggregate Turnover | Registration Required | Applicability |

|---|---|---|

|

Earlier Limits for Goods/Services |

||

|

Exceeds ₹20 lakh |

Yes – Normal Category States |

Upto 31 March 2019 |

|

Exceeds ₹10 lakh |

Yes – Special Category States |

Upto 31 March 2019 |

|

Revised Limits for Sale of Goods |

||

|

Exceeds ₹40 lakh |

Yes – Normal Category States |

From 1 April 2019 |

|

Exceeds ₹20 lakh |

Yes – Special Category States |

From 1 April 2019 |

|

Revised Limits for Providing Services |

||

|

Exceeds ₹20 lakh |

Yes – Normal Category States |

From 1 April 2019 |

|

Exceeds ₹10 lakh |

Yes – Special Category States |

From 1 April 2019 |

Turnover Limits For GST Registration

Businesses with an annual turnover exceeding ₹40 lakhs for goods and ₹20 lakhs for services are required to register for GST and meet their tax obligations on taxable goods and services. However, businesses with annual revenue below ₹40 lakhs have the option to voluntarily register for GST. Opting for registration, even when not mandatory, allows these businesses to avail themselves of benefits such as input tax credit. It is important to note that states categorized as special category states have different minimum thresholds, set at ₹10 lakhs for services and ₹20 lakhs for goods. Below is a detailed outline of these thresholds.

| Category | States/Union Territories Included |

|---|---|

|

Normal Category States/UTs Opting for ₹40 Lakh Limit |

Kerala, Chhattisgarh, Jharkhand, Delhi, Bihar, Maharashtra, Andhra Pradesh, Gujarat, Haryana, Goa, Punjab, Uttar Pradesh, Himachal Pradesh, Karnataka, Madhya Pradesh, Odisha, Rajasthan, Tamil Nadu, West Bengal, Lakshadweep, Dadra and Nagar Haveli and Daman and Diu, Andaman and Nicobar Islands, and Chandigarh. |

|

Normal Category States Opting for Status Quo (No ₹40 Lakh Limit) |

Telangana |

|

Special Category States/UTs Opting for ₹40 Lakh Limit |

Jammu and Kashmir, Ladakh, and Assam |

|

Special Category States/UTs Opting for ₹20 Lakh Limit |

Puducherry, Meghalaya, Mizoram, Tripura, Manipur, Sikkim, Nagaland, Arunachal Pradesh, and Uttarakhand. |

Did You Know?

As of 30 November 2023, India had a total of 1 crore 40 lakhs approximately active taxpayers registered under GST across different states and registration categories. If you haven’t registered your business yet, now is the perfect time! Simplify the process and get your firm GST-registered effortlessly with Covering Taxes. Take advantage of our expert assistance to ensure a seamless experience.

What is Form GST REG-01?

Form GST REG-01 serves as the application form required for obtaining Goods and Services Tax (GST) registration in India. Any individual or entity eligible for GST registration must complete and submit this form. It is particularly important for newly registered taxpayers under GST, as it enables them to claim Input Tax Credit (ITC) on stock held prior to registration. Filing this form is a crucial step to ensure compliance with GST regulations and to avail ITC benefits. However, it excludes specific categories such as non-resident taxable persons, those required to deduct tax at source under Section 51, collect tax at source under Section 52, or supply online services, as they follow separate registration procedures in accordance with Rule 8(1) of the GST rules..

GSTIN and It’s Significance

The GSTIN (Goods and Services Tax Identification Number) is a unique 15-digit code assigned to businesses and entities registered under the Goods and Services Tax (GST) system in India. This number is used to identify taxpayers, such as dealers, suppliers, and other business entities, across the country. The introduction of GSTIN ensures better transparency within the GST framework, making it easier for authorities to track and manage tax data, thereby reducing tax evasion. For small businesses, having a GSTIN opens the door to several advantages, including access to government support programs, the ability to claim Input Tax Credit (ITC) on purchases, and enhanced trust with both suppliers and customers. The GSTIN is also essential for various business activities, including applying for loans, claiming GST refunds, facilitating verification processes, correcting errors in GST filings, and managing the overall tax identification process.

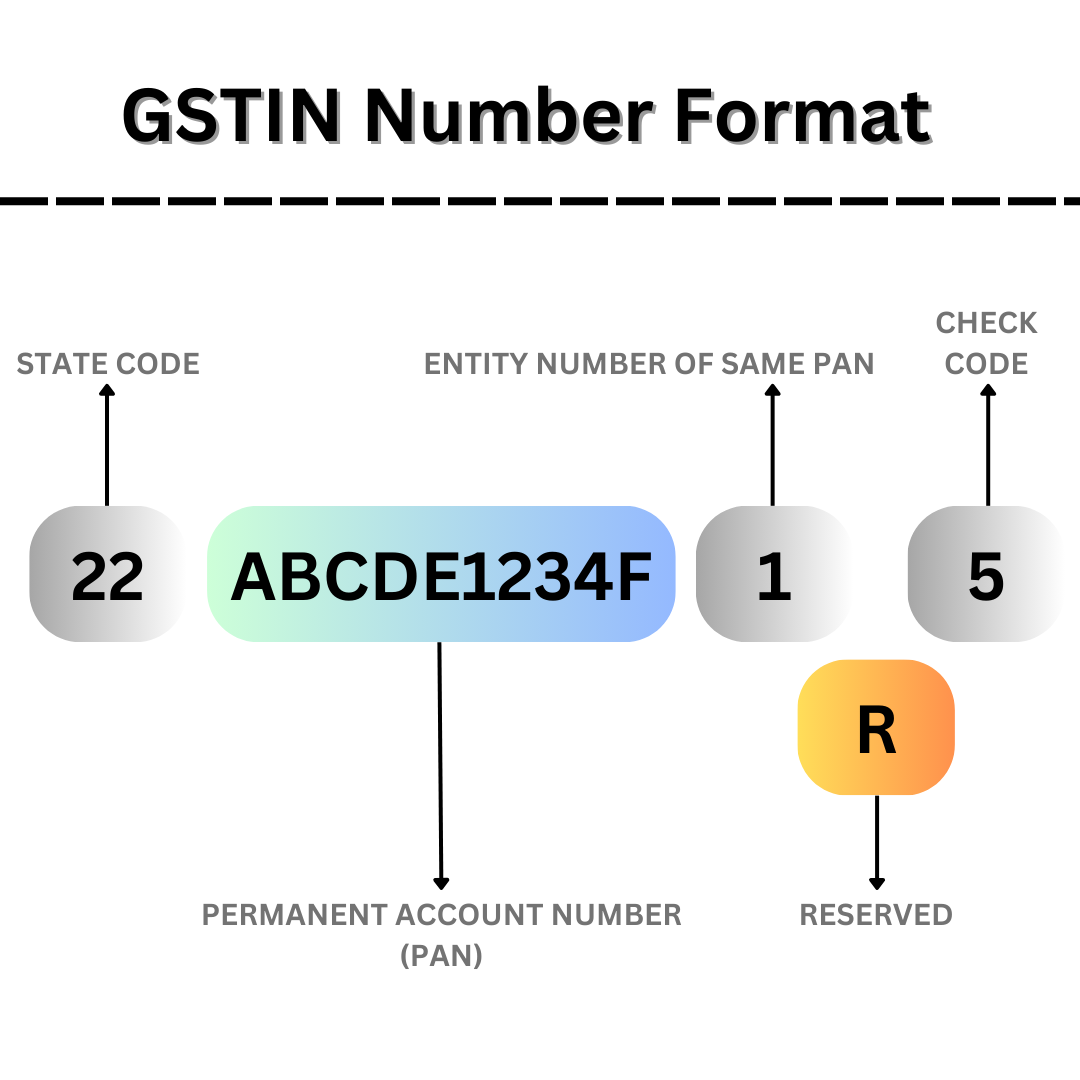

Understanding Your GST Identification Number (GSTIN)

A GSTIN (Goods and Services Tax Identification Number) is a unique 15-character code issued to businesses registered under the GST system in India. This number plays a vital role in identifying businesses for tax purposes and streamlining GST-related transactions. Here’s a breakdown of the GSTIN structure:

State Code (First Two Digits):

The first two digits represent the state code where the business is registered. For example, “22” indicates registration in Uttarakhand.PAN Number (Next Ten Digits):

The next ten digits correspond to the Permanent Account Number (PAN) of the business or taxpayer. This is used to uniquely identify the business entity. For example, “ABCDE1234F” is an example of a PAN.Entity Code (Next One Digit):

The thirteenth digit represents the entity code, which defines the type of taxpayer. For most businesses, this will be “1,” indicating a sole proprietor or individual business.Reserved Field (Next One Digit):

The fourteenth digit is currently reserved for future use and remains blank for now.Check Code (Final Digit):

The last digit is a check code used to validate the authenticity and accuracy of the GSTIN.

This structured format ensures that the GSTIN is both accurate and traceable, allowing businesses to comply with the GST laws and facilitate smooth tax-related operations.

Consequences of Not Registering for GST

Failing to register for GST, as mandated by the Goods and Services Tax Act of 2017, can lead to significant penalties. If a business or individual is required to register under GST but neglects to do so, they could face a fine of ₹10,000 or an amount equal to the tax evaded or any shortfall in the taxes due, whichever is higher, according to Section 122 of the CGST Act. Additionally, the penalty for non-registration can be as high as ₹2 lakh, or ₹10,000, whichever amount is greater. This emphasizes the importance of timely GST registration to avoid such financial consequences.

Penalties for Non-Compliance with GST Regulations

Non-compliance with GST regulations can lead to several penalties. These include:

Late Filing Penalty: If GST returns are filed after the due date, a penalty for late filing will be imposed.

Interest on Outstanding Tax: Interest will be charged on any unpaid GST liabilities that are due, increasing the overall amount owed.

Suspension or Cancellation of GST Registration: Failure to follow GST rules could result in the suspension or cancellation of your GST registration, affecting your ability to conduct business.

Penalty for Non-Compliance: The penalty for non-compliance can be up to 10% of the total tax amount due. In addition to this, penalties may be imposed for each instance of non-compliance.

Interest on Overdue Taxes: The taxpayer is also liable to pay interest on any overdue taxes, which adds to the financial burden.

These penalties highlight the importance of adhering to GST rules and filing returns on time to avoid unnecessary financial penalties and disruptions to business operations.

Mandatory GST Registration for Specific Businesses

Certain businesses must obtain GST registration, regardless of whether they meet the threshold limit. These include:

Interstate Taxable Supply: Individuals engaged in interstate taxable supply of goods or services, with a threshold limit of ₹20 lakhs for goods and ₹10 lakhs for services.

Casual Taxable Persons: Businesses that conduct taxable supplies on a casual basis, such as temporary or seasonal businesses.

Reverse Charge Mechanism: Individuals who are obligated to pay tax under reverse charge for inward supplies received.

Non-Resident Taxable Persons: Non-residents involved in taxable supplies in India must register for GST.

E-Commerce Entities: This includes all e-commerce operators and any individual supplying goods or services through an e-commerce platform.

Tax Deduction at Source (TDS): Individuals required to deduct tax under Section 51 of the GST Act.

Input Service Distributors: Entities engaged in the distribution of input services.

Supplies on Behalf of Other Taxable Persons: Individuals making taxable supplies of goods or services on behalf of other taxable persons, including agents.

Section 9(5) Taxpayers: Persons required to pay tax under Section 9(5), which pertains to specified services provided by the government.

Other Categories: Any other individuals or categories as notified by the government.

Types of GST Returns and Their Due Dates in 2024

Here is a clear outline of different GST returns and their due dates in 2024:

| Return/Form | Description | Frequency | Due Date | Applicable Period |

|---|---|---|---|---|

|

GSTR-1 |

Details of outward supplies of goods or services |

Monthly |

11th of the following month |

April 2024 – March 2025 |

|

|

|

Quarterly |

13th of the month following the quarter |

April-June 2024, July-September 2024, October-December 2024, January-March 2025 |

|

GSTR-3B |

Summary return of outward supplies, input tax credit, and payment of tax |

Monthly |

20th of the following month |

April 2024 – March 2025 |

|

|

|

Quarterly |

22nd or 24th of the month following the quarter (depending on the state) |

April-June 2024, July-September 2024, October-December 2024, January-March 2025 |

|

CMP-08 |

Statement-cum-challan for composition taxpayers |

Quarterly |

18th of the month following the quarter |

April-June 2024, July-September 2024, October-December 2024, January-March 2025 |

|

GSTR-4 |

Annual return for composition taxpayers |

Annually |

30th April 2025 |

FY 2024-25 |

|

GSTR-5 |

Return for non-resident foreign taxpayers |

Monthly |

13th of the following month |

April 2024 – March 2025 |

|

GSTR-6 |

Return for input service distributors |

Monthly |

13th of the following month |

April 2024 – March 2025 |

|

GSTR-7 |

Return for authorities deducting tax at source (TDS) |

Monthly |

10th of the following month |

April 2024 – March 2025 |

|

CGSTR-8 |

Return for e-commerce operators collecting tax at source (TCS) |

Monthly |

10th of the following month |

April 2024 – March 2025 |

|

GSTR-9 |

Annual return for regular taxpayers |

Annually |

31st December 2025 |

FY 2024-25 |

|

GSTR-9C |

Reconciliation statement and certification for taxpayers with turnover above ₹5 crore |

Annually |

31st December 2025 |

FY 2024-25 |

|

GSTR-10 |

Final return upon cancellation of GST registration |

Once |

Within three months of the cancellation date or order, whichever is later |

As applicable |

|

GSTR-11 |

Return for taxpayers with Unique Identification Number (UIN) |

Monthly |

28th of the following month |

April 2024 – March 2025 |

Key Errors to Avoid During GST Registration and Compliance

Insufficient Documentation Management

One of the primary missteps in GST registration is the failure to maintain accurate and systematic records, including invoices, purchase bills, and supply records. Proper documentation forms the backbone of GST compliance, ensuring smooth filing processes and reducing the chances of errors or penalties.

Errors in Invoice Details

Mistakes such as an incorrect GST Identification Number (GSTIN), mismatched invoice numbers, or improper tax computation can lead to severe compliance issues. Ensuring precision in invoice preparation and verification is essential to maintain compliance and avoid penalties.

Mismatch Between GSTR-2A and GSTR-3B Data

Neglecting to reconcile purchase details reflected in GSTR-2A with the summary return filed in GSTR-3B is a common pitfall. Such mismatches can result in compliance breaches and disputes over claiming Input Tax Credit (ITC), potentially impacting your tax liabilities.

Non-Adherence to Return Filing Deadlines

Delays in filing GST returns often attract penalties and interest. Staying updated with the due dates and filing returns promptly not only ensures compliance but also avoids unnecessary financial strain.

Failure to Verify Supplier GSTINs

Verifying the authenticity of suppliers’ GSTINs through the GST portal is critical. Transactions with suppliers using fake or invalid GSTINs can result in the denial of Input Tax Credit (ITC), adversely affecting your tax standing and business finances.

Limited Knowledge of the GST Composition Scheme

A lack of understanding of the GST Composition Scheme can lead to incorrect filings and non-compliance. Small businesses eligible for the scheme should fully grasp its conditions, benefits, and limitations before opting for it to ensure accuracy in their GST submissions.

Ignoring GST Authority Notices

Disregarding notices or non-compliance alerts from GST authorities can lead to legal disputes and heavy fines. It is crucial to promptly address any communication from the authorities to mitigate risks and maintain regulatory compliance.

Step-by-Step Guide In Completing GST Registration

- STEP 1 - Get in touch with the experts

- STEP 2 -Provide Business Information

- STEP 3 - Filing for GST Registration

- STEP 4- Get Your GSTIN

Registering for GST involves a straightforward process that ensures your business complies with tax regulations. Here’s how you can complete it in four simple steps:

Step 1: Connect with Our GST Experts

Start by booking a consultation with our experienced GST advisors. This session will address all your queries and provide clarity on the GST registration process tailored to your business needs.

Step 2: Submit Business Information

Provide the necessary details and documents to initiate your application. Key information includes:

- Business Name

- SEZ Unit Status (if applicable)

- Principal and Additional Places of Business

- Mobile Number and Email Address

- PAN Card Details

- State of Operation

Ensure that all documents are accurate and align with government requirements to prevent delays.

Step 3: Filing Your GST Application

Our team will file the GST registration application on the official GST portal. During this process:

- An OTP will be sent to your registered mobile number for verification.

- Verification ensures the accuracy of the details provided.

Step 4: Receive Your GSTIN

Once the application is successfully verified, you will receive an Application Reference Number (ARN), which acts as a temporary reference for tracking your registration status. Upon approval:

- The GST Registration Certificate will be issued by the Central Government.

- The GST Identification Number (GSTIN) will be accessible on the GST portal.

Note: It is crucial to adhere to submission timelines and provide accurate information. At Covering Taxes, we will guide you throughout the process, ensuring seamless registration and prompt receipt of your GST certificate.

Frequently Asked Questions

A: Absolutely! Even if your annual turnover falls below the mandatory threshold, you can opt for voluntary GST registration. This decision can be advantageous as it enables you to claim input tax credits, engage in interstate trade, and boost your business’s credibility in the market.

A: Delaying GST registration can result in monetary penalties, including late fees and interest on unpaid taxes. Timely registration is essential to avoid these financial setbacks and to maintain compliance with the tax laws.

A: The effective date of GST liability marks the point when your obligation to collect and pay GST begins, based on your turnover or business activities. On the other hand, the registration approval date is when your GST application is officially processed and accepted. Knowing the distinction helps you determine the timeline for fulfilling your GST responsibilities.

A: Absolutely. Once you voluntarily register for GST, you must issue GST-compliant invoices and collect the applicable taxes on your sales. This ensures compliance with GST laws, even if your turnover is below the prescribed limit, and promotes transparency in your business dealings.

A: No, claiming input tax credit is not permitted for goods sold at a 5% GST rate by your LLP. Input tax credit is generally applicable to higher GST rates, and transactions under the concessional 5% rate do not qualify for this benefit in such cases.

A: Businesses that are unregistered for GST and engage with GST-compliant suppliers should consider obtaining GST registration. Without registration, the business cannot claim input tax credits and must absorb the full tax cost, which could negatively affect profitability and financial efficiency.

A: To fix the SB001 error during GST export via ICEGATE, ensure that all submitted details are accurate and match the export documentation. Double-check shipping bill information, GSTIN, and invoice data for discrepancies. If the issue persists, reach out to ICEGATE or GST helplines for expert assistance in resolving technical glitches efficiently.

A: To resolve negative amount issues in GSTR-3B arising from credit notes, ensure the values are corrected in the relevant fields. Any discrepancies should be reported in the following return periods. Keep meticulous records of credit notes to help reconcile any errors and prevent issues in future filings.

A: If your GSTIN has been cancelled and the final return was not filed, it’s crucial to submit the pending return as soon as possible. Neglecting this step may result in penalties and complications with your GST compliance. Act quickly to resolve the issue and avoid further consequences.

A: The GST Annual Return is a comprehensive report that outlines a business’s total GST-related transactions for the financial year. It includes key information such as sales, purchases, and the taxes paid during the year. This return serves as a summary of the taxpayer’s GST compliance and helps ensure accuracy in reporting throughout the year.

A: The HSN Code, which stands for Harmonized System of Nomenclature, is a globally accepted classification system for products. It helps identify and categorize goods for taxation and trade compliance purposes, facilitating efficient customs procedures and trade between countries. By assigning unique codes to products, it ensures consistency and transparency in international trade.

A: SAC Code stands for “Service Accounting Code.” It is a unique code used to categorize services under the GST framework. This classification helps in streamlining tax rates and ensures consistent application of tax across various service sectors, making the process easier for businesses and service providers to comply with GST regulations.

A: Absolutely! A salaried person can register for GST if they are engaged in any business or entrepreneurial activity outside of their regular employment. GST registration becomes compulsory if their annual turnover exceeds the specified threshold limit set by the government.

A: An E-way Bill is an electronically generated document that authorizes the transportation of goods exceeding a specified value, particularly when goods are being transported across state borders. It serves as a compliance tool, ensuring proper tax documentation and facilitating hassle-free movement of goods by outlining key consignment details.